Global Earnings Growth: Broadening Beyond Technology

Corporate earnings expectations are strengthening — and not just at the margins. Compared with the already constructive outlook from recent quarters, the direction of travel is clearly upward across the next two years. What's notable is wherethe momentum is coming from: increasingly, it's from beyond US large-cap growth and the Magnificent Seven.

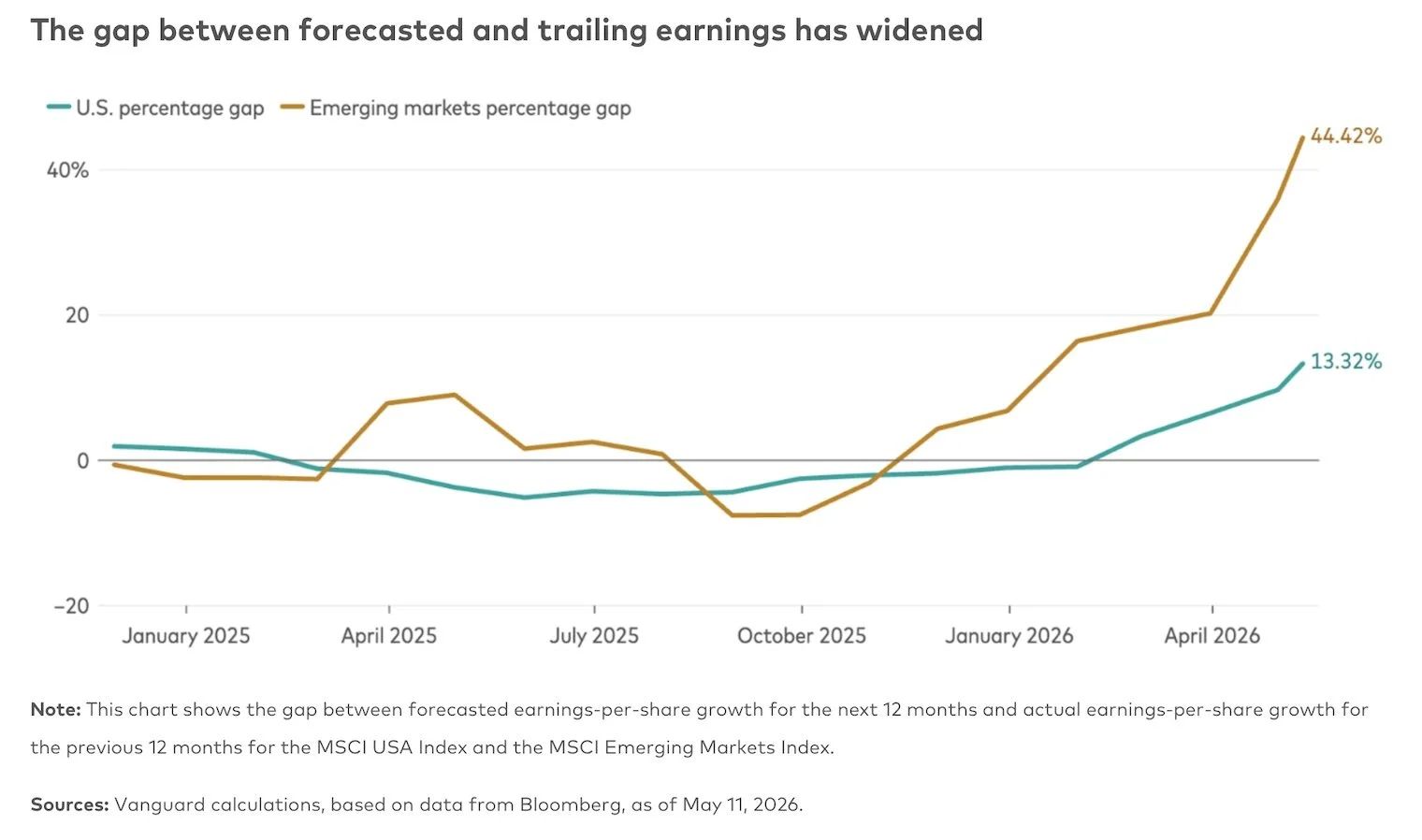

Earnings growth is running measurably ahead of the recent historical pace, and crucially, it's broadening. The most pronounced improvement in forward earnings expectations — relative to trailing actuals — is visible in small-cap, value, and emerging market equities. US growth stocks and the Magnificent Seven, while still solid, are seeing comparatively more modest revisions. The gap between forecast EPS growth for the next 12 months and actual EPS growth for the prior 12 months is widening across both US and emerging market equities — a meaningful signal of shifting dynamics.

The AI Buildout Is the Engine

At the heart of this broader earnings momentum is the AI capital expenditure cycle. Hyperscalers — the major technology companies building and operating large-scale, AI-optimised cloud infrastructure — are estimated to deploy approximately US$800 billion in AI-related capital spending this year alone. That spending is already flowing through to earnings beats across the global AI infrastructure supply chain, encompassing lithography, foundry, memory, and storage within semiconductor manufacturing.

Increasingly, market attention is concentrating on what has emerged as the critical bottleneck: high-bandwidth memory chips. These are essential for inference-heavy workloads and AI agents, where latency — the delay between an AI input and its output — is a competitive differentiator. The focus on high-bandwidth memory is translating into exceptional earnings growth and rising expectations for companies including Micron Technology and SanDisk in the US, and SK Hynix and Samsung in Korea, alongside strong price performance.

The Ripple Effects Are Wide

The impact of AI investment is not confined to semiconductors. The physical demands of building, powering, and cooling data centres are generating meaningful earnings tailwinds across energy, utilities, industrials, and materials. And the second-order effects are still unfolding: as AI diffuses more broadly through the economy, productivity gains should begin to lift earnings and margins well beyond the immediate infrastructure ecosystem.

The Questions That Will Shape What Comes Next

How this plays out will hinge on three key issues:

Will AI infrastructure spending continue to strengthen, sustaining earnings momentum in semiconductors and Korea- and Taiwan-linked equities?

How effectively will the major hyperscalers — Amazon, Alphabet, Meta, and Microsoft — monetise their substantial AI investment?

Will early indications of AI adoption begin to materially lift earnings and margins across the broader economy?

These are not peripheral questions. They are the variables most likely to define the earnings growth profile of global equity markets over the medium term — markets that have already been fundamentally shaped by AI, and will continue to be.

Rick Maggi CFP, Financial Advisor Perth, Westmount Financial

_____________________________________________________

Disclaimer: Important Information:

All investing is subject to risk, including possible loss of principal.

Investments in stocks or bonds issued by non-US companies are subject to risks including country/regional risk and currency risk. These risks are especially high in emerging markets.

Prices of mid- and small-cap stocks often fluctuate more than those of large company stocks.

The example is illustrative only and is based on the factors stated. It should not be taken to contain or provide an estimate or forecast of the gap between forecasted earnings-per-share growth for the next 12 months and actual earnings-per-share growth for the previous 12 months.

This article contains certain 'forward looking' statements. Forward looking statements, opinions and estimates provided in this article are based on assumptions and contingencies which are subject to change without notice, as are statements about market and industry trends, which are based on interpretations of current market conditions. Forward-looking statements including projections, indications or guidance on future earnings or financial position and estimates are provided as a general guide only and should not be relied upon as an indication or guarantee of future performance. There can be no assurance that actual outcomes will not differ materially from these statements. To the full extent permitted by law, Vanguard Investments Australia Ltd (ABN 72 072 881 086 AFSL 227263) and its directors, officers, employees, advisers, agents and intermediaries disclaim any obligation or undertaking to release any updates or revisions to the information to reflect any change in expectations or assumptions.

The funds or securities referred to herein are not sponsored, endorsed, or promoted by MSCI, and MSCI bears no liability with respect to any such funds or securities. The prospectus or the Statement of Additional Information contains a more detailed description of the limited relationship MSCI has with Vanguard and any related funds.

BLOOMBERG®” and the Bloomberg indices listed herein (the “Indices”) are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the Indices (collectively, “Bloomberg”) and have been licensed for use for certain purposes by the distributor hereof (the “Licensee”). Bloomberg is not affiliated with Licensee, and Bloomberg does not approve, endorse, review, or recommend the financial products named herein (the “Products”). Bloomberg does not guarantee the timeliness, accuracy, or completeness of any data or information relating to the Products. ©2026 Bloomberg. Used with Permission.